Welcome to your investor update. This series is to keep you up to date on the scheme, the markets, and investment topics to help you get the most out of your KiwiSaver investment.

In this edition, we are talking about saving during a cost-of-living crisis.

Saving during a cost-of-living crisis

One of the great features of KiwiSaver is that it keeps the discipline of saving going even when times are a feeling a little tougher.

With prices for necessities rising across the board, keeping on track with your savings goals (particularly long-term goals like retirement) can seem more difficult than ever before. The regular amount that you put aside each payday can become less consistent, or your fixed monthly savings goal is coming up a little short each time. It takes willpower to keep up with good financial habits when things are tight.

If you are struggling with sticking to your other long-term savings plans and keeping your discipline in place, your KiwiSaver account may be ideal savings product for you. As your contributions are automatically deducted from your pay, this takes willpower out of the equation.

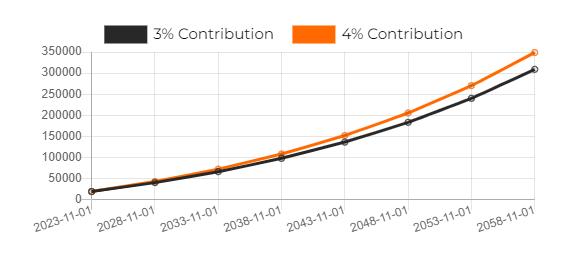

Moving your contribution rate from 3% to 4% is a relatively small increase per payday, but over the long-term this increase can really add up.

For example, in the case of a 30-year-old aggressive investor earning $50,000 per year and with a $20,000 current balance, that 1% per year (about $9 per week i.e. less than 2 coffees) could add up to $40,000 more in savings at the age of retirement*.

You can use our calculator here to see the impact of increasing your contributions using your own information – you may be surprised by how big the difference the higher contribution rates can make. Increasing your contributions is really easy and can be done though your employer or the IRD here.

As always, you can contact our team of Financial Advisers to talk about your Lifestages account – there’s no additional cost to you as a member. They can help you make the right decisions for your personal circumstances.

*This was calculated using the Lifestages Retirement Calculator for a 30-year-old investor in an aggressive KiwiSaver profile. The investor was assumed to be earning $50,000 per year with an existing balance of $20,000 and a 3% employer contribution. You can find more about how our Lifestages Retirement Calculator works here.

Performance Overview

The Lifestages Auto Options invest in combinations of the Lifestages High Growth Fund and the Lifestages Income Fund in proportions that vary in accordance with pre-selected age bands. These options automatically adjust the risk profile of your investment by altering the proportions invested into the funds based on your age.

Performance as at 31 October 2023.

| Fund Option | 1M | 1Y | 5Y |

| High Growth Fund | -2.12% | 6.88% | 6.09% |

| Auto 0-49 Option | -2.12% | 6.88% | 6.09% |

| Auto 50-54 Option | -1.78% | 5.75% | 5.00% |

| Auto 55-59 Option | -1.44% | 4.61% | 3.84% |

| Auto 60-64 Option | -1.10% | 3.45% | 2.65% |

| Auto 65+ Option | -0.93% | 2.84% | 1.78% |

| Income Fund | -0.42% | 1.10% | 0.14% |

For more information about how performance is calculated and more performance periods, click here.

Market Update

Markets continued to remain volatile through October. This was largely due to newly emerging conflicts increasing geopolitical risk, a further increase in long-term interest rates, and several company’s share prices reacting to economic growth weakness.

Volatile markets are not uncommon, particularly within share investments, but fixed-interest investments are also not immune from these ups and downs. The benefit of volatility is that it demands a return premium relative to holding cash in the bank – meaning you receive a better overall return over the long term. Historically this premium ranges from around 1% per annum for fixed interest to 4-5% per annum for shares.

However, despite the recent difficulties in the market, the outlook is looking a little more positive. Fixed interest rates are at their highest level for 10 years, and company share valuations are starting to look attractive for the first time this year.