The launch of ChatGPT in late 2022 set off one of the fastest and biggest capital expenditure cycles in decades.

So far, this has been led by US Big Tech companies, with much of the spend being pumped into the buildout of the necessary infrastructure to provide computing power for AI models.

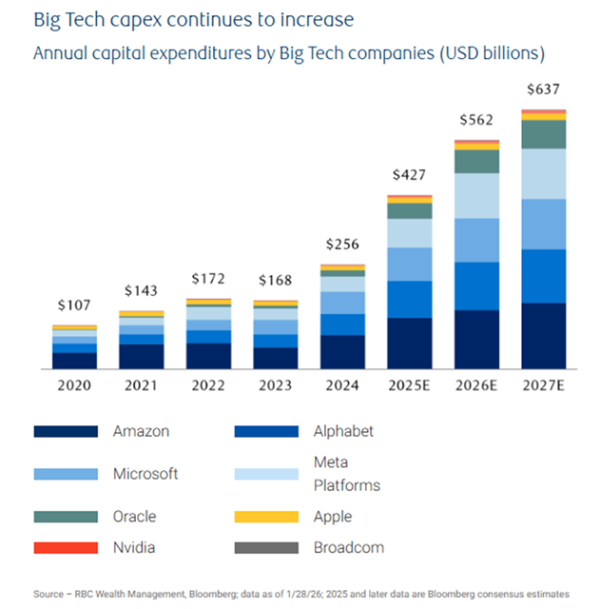

Data centres, semiconductors and networking equipment are benefitting from the unprecedented pace of spending with capital expenditure of US Big Tech firms doubling over the last two years, reaching approximately USD$427 billion in 2025. This momentum is expected to continue into 2026 and beyond with estimates pointing to increases of up to another 30 percent this year alone (USD$562 billion).

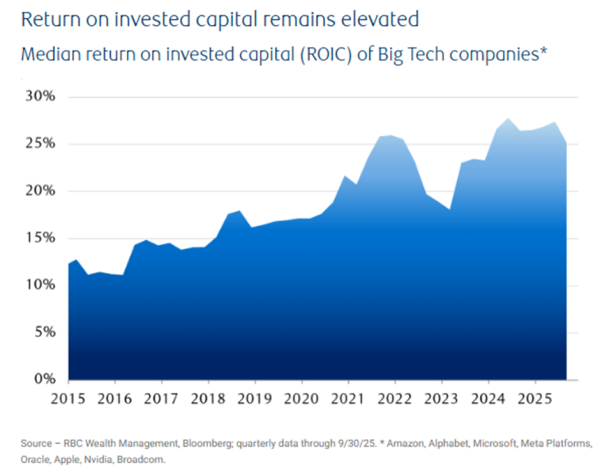

Investors have begun to wonder just how long this level of capital spending can hold up, questions that are somewhat justified in the current market environment. However, the major AI spenders (Amazon, Google, Meta, Microsoft, Apple, Broadcom, and Oracle), are generally seen as being in sturdy financial positions – underscored by cash-rich balance sheets and solid cash flow generation abilities.

As of the end of September last year, these companies held a combined USD$490 billion in cash and equivalents and together generated USD$400 billion in trailing 12-month free cash flow after capital expenditure outlays. This implies that most of the AI-related spending was funded by internally generated cash.

This evidence of strong self-financing capacity suggests that the current level of investment can be sustained for the foreseeable future. However, a material slowdown in earnings growth could heighten the market’s scrutiny and test the tolerance for a continuation of this level of spending. We believe however, that the more recent trend of companies utilising debt financing to fuel AI spending, helps to mitigate this risk.

As we covered in the last edition of Basis Points, US Big Tech companies continue to maintain earnings momentum above that of the broader market, which helps give us further confidence in this theme.

The Data Centres & Smart Infrastructure investment theme is the second link in the AI value chain following on from our last Basis Points edition on AI & Automation. Next time, we move on to the next link: Electrification & Climate Action.

What we’re reading: Message from JLL Assistant